[ad_1]

Disclaimer: This isn’t funding recommendation. PLEASE DO YOUR OWN RESEARCH !!!

– A Hidden French Compounder that is as exciting as watching Paint dry ?")

As prior to now, as a result of dangerous WordPress editor, I’ll publish a abstract right here and connect the complete write-up as PDF.

After teasing a brand new place within the Nabaltec “Submit Mortem”, I proudly current the subsequent (hopefully) tremendous boring firm for my boring portfolio.

SAMSE SA is a French firm that distributes constructing supplies to “skilled” prospects like contractors, craftsmen and so on. It additionally has a smaller “Direct to shopper” DYI retailer section, which represents round 20% of gross sales. Samse is lively solely in France and No. 2 after Saint Gobain, which, nevertheless is way greater even solely on this particular sector (2000 shops vs. 350).

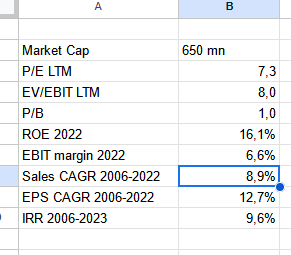

Right here is an summary of related “KPIs” at a share worth of 190 EUR (time of writing):

PDF file with detailed write-up:

Professional’s and Con’s

What do I like:

Household owned/managed

Exceptionally excessive worker possession

Conservative monetary profile and enterprise mannequin

Countercyclical M&A

Decentralized group

Excellent firm tradition

enterprise that I form of perceive (distribution)

not enticing at first sight

potential “mushy catalyst” by acquisition in powerful occasions

cheap valuation

Dangers

Nonetheless Leverage on Holdco degree

perhaps over incomes in 2021 and 2022

Cycle in constructing supplies may nonetheless worsen

low free float

provides to my sector publicity (Thermador, Sto, Photo voltaic)

For some motive, they’ve discontinued English experiences from 2018 onwards

Abstract:

SAMSE appears to be a kind of prime quality “hidden Champion” firms that I’m all the time searching for. The enterprise is extraordinarily boring and topic to financial cycles. Alternatively, the corporate appears to be very properly managed they usually appear to have the ability to use the cycles to get out stronger from the lows than they entered.

I made a decision to allocate a 3% place into SAMSE at a mean worth of 190 EUR per share, funded primarily by the sale of the Nabaltec place. The three% displays my present publicity to the sector.

Truthfully, I don’t anticipate an ideal and fast run up of the share worth. I really hope that the share worth does little or no and that I can add if fundamentals slowly get higher over time like within the Schaffner and Meier Tobler case.

Sources:

A giant thanks particularly to Jeremy from “French Hidden Champions” and Philippe Luchesi. Each guys are price following in case you are occupied with high quality French shares.

Philippe on SAMSE:

Jeremy on SAMSE:

https://frenchhiddenchampions.substack.com/p/sfaf-analyst-meeting-report-samse?s=w

A current interview with the CEO:

[ad_2]

Source link