[ad_1]

gremlin

Funding motion

I advisable a maintain score for Hubbell Integrated (NYSE:HUBB) once I wrote about it the final time (third Dec 2023), because the HUBB valuation was not buying and selling at a beautiful degree. Nevertheless, HUBB has exceeded my expectations, beating my FY23 estimates. Primarily based on my present outlook and evaluation of HUBB, I like to recommend a purchase score. I count on a 1-year return of 12% for HUBB primarily based on my present goal value. Not like my earlier put up, I’m fairly assured that HUBB can meet or beat its FY24 steerage given the present outlook and the conservatism embedded within the information.

Evaluate

HUBB reported very robust outcomes for 4Q23 on thirtieth Jan, the place gross sales got here in at $1.35 billion, rising 10%. Development was led by each segments: electrical and utility development of 6% and 13%, respectively. Sturdy development was adopted by a stronger section revenue development of 34%, pushed by each segments and margin enchancment from ~16% to ~19%. EPS noticed a stronger leap from $2.60 in 4Q22 to $3.69 in 4Q23. On a full-year foundation, the highest line noticed 8.6% development to $5.37 billion in gross sales, EBIT got here in at ~$1 billion, which was a ~42% development FY22, and EPS got here in at $14.44 vs. 9.62 final 12 months.

HUBB

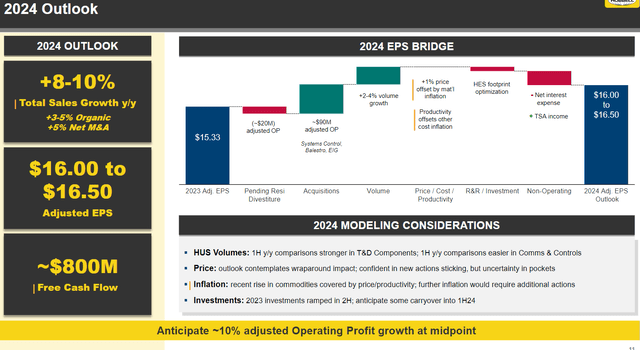

Taking a look at how HUBB carried out in 4Q23, I imagine there’s a good probability for HUBB to fulfill FY24 steerage if the momentum continues. Particularly, administration is guiding natural development of 3-5%, pushed by 3% quantity on the midpoint (2 to 4%) and 1% value, and M&A to contribute one other 5%, bridging to ~10% development for FY24. Within the under sections, I’ll break down every a part of this steerage equation to debate what drove the change in thoughts that HUBB can meet this information.

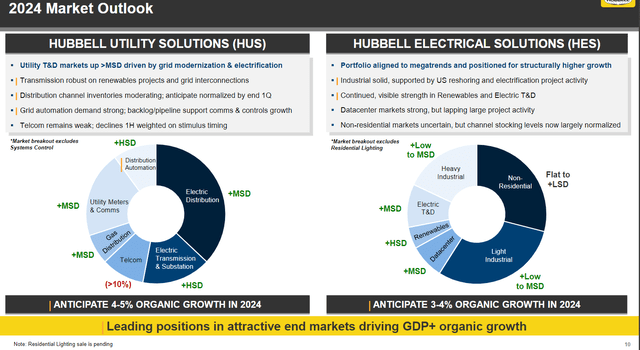

Beginning with quantity development, finish market demand developments at each electrical and utility proceed to pattern nicely, as administration has not referred to as out any demand shifts since 3Q23. The outlook stays optimistic, the place utility T&D (transmission and distribution) markets are anticipated to be up extra, a minimum of by mid-single-digits, pushed by power in T&D. I imagine this outlook for the utility section has excessive creditability, however the backlog remains to be at an elevated degree, which supplies visibility. As for {the electrical} section, the outlook additionally stays optimistic, with a principally mid-single-digit development outlook for all its finish markets. In my opinion, I feel administration steerage for {the electrical} section is on the conservative facet, which implies there may be risk for a beat. Within the presentation slide, they famous the non-resi market as unsure, but in addition famous that channel stocking ranges have normalized. From the decision, we will infer that this section noticed a low-single-digit affect from destocking in FY23. This additionally signifies that the flat-to-low-single-digit information is actually from the straightforward FY23 comp (since FY24 won’t have the identical destocking concern). If the macro state of affairs recovers, it’s probably that the non-resi section outperforms expectations—a potential upside catalyst.

HUBB

Secondly, relating to pricing, I feel the 1% information is definitely achievable provided that it contains carryover from FY23 value actions and that FY24 pricing motion will proceed to profit from uncooked materials inflation. Thus far in January, administration has famous that the market has been receptive to its pricing actions. This has a deeper implication that means potential increased pricing development than 1%. If we have a look at HUBB historic pricing development, it averages to be about 2% from FY04 to FY23. Assuming that HUBB is ready to revert again to this common pricing development, say 50% of this pricing is realized in FY24 (the remaining is realized in FY25), this already implies a 1% development. Including the advantages of FY23 value actions, value development for FY24 might exceed the 1% guideline.

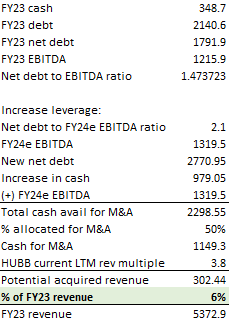

Lastly, for M&A development, I imagine it’s a matter of stability sheet power. As of 4Q23, HUBB has a internet debt place of round $1.8 billion, or 1.5x internet debt to EBITDA. It is a very snug vary for HUBB, as it’s on the midpoint of its current low of 1x and excessive of two.1x. HUBB has been a serial acquirer for a while now, making a minimum of 16 recognized public acquisitions since FY12. All through this era, the implied value to gross sales ratio is often ~1.3 to 1.6x (primarily based on HUBB historic filings), which provides me some confidence that they won’t overpay by an enormous quantity. Even when assuming that HUBB doesn’t make an acquisition that’s buying and selling increased than its personal valuation (~3.8x LTM income), I imagine the 5% M&A contribution is believable. Administration additionally particularly referred to as out that the M&A pipeline stays strong, so I might not be too anxious concerning the variety of targets obtainable. Beneath is my math:

Writer’s work

On the backside line, administration guided for an adjusted EPS vary of $16 to 16.50, which means a internet earnings determine of ~$880 million on the midpoint, beating my authentic FY24 estimate of $853 million. In my opinion, an enormous a part of this anticipated outperformance is that HUBB goes to see margin advantages from the sale of Resi Lighting. The Resi Lighting section generated $228 million in FY22 and $190 million in FY23, which is round 10% of the Electrical energy section. This enterprise has a low double-digit share margin, so from a mixture perspective, the consolidated margin ought to enhance with out it.

Valuation

Writer’s work

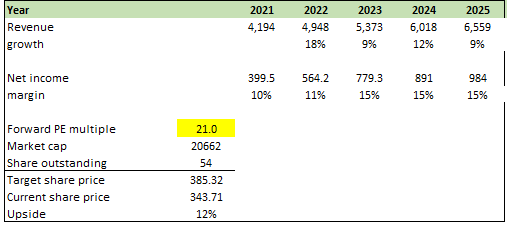

I imagine HUBB can develop at 12% in FY24 (vs my earlier expectation of 14% for FY24) and 9% in FY25. My development estimate for FY24 is increased than steerage as a result of I see potential for outperformance in non-resi (electrical) if the macro surroundings recovers, with higher pricing and the next M&A development contribution. In FY25, development ought to begin to normalize again to historic development of mid-single-digits (9% is the midpoint). For internet margin, I count on HUBB to hit the excessive finish of its guided vary ($16.5 EPS), as a consequence of causes I mentioned above that led me to imagine HUBB will see outperformance on the prime line (vs my expectation of $853 million for FY24 beforehand). Because the outlook appears to be vivid, I imagine the market will proceed to worth HUBB at 21x for this 1-year interval. Therefore, I’ve a value goal of $385 by FY24e.

Danger and remaining ideas

A giant a part of the expansion equation is M&A, and lots of issues might occur to steer this off beam. As an illustration, the asking value is just too costly, the price of capital will get dearer if the Fed doesn’t minimize charges, and a deteriorating macro surroundings would additionally restrict HUBB’s capability to be extra aggressive as they must be extra cautious. I feel the one approach to monitor this rate of interest threat is by monitoring the important thing indicators (inflation and unemployment) which might be launched month-to-month to get a way of the present financial system state of affairs.

To conclude, I’m upgrading HUBB to a purchase score, anticipating a 12% 1-year return primarily based on a sturdy FY24 outlook. The forecasted 3-5% natural development, conservative electrical section steerage, achievable pricing development goal, and a powerful stability sheet led me to imagine that assembly/beating FY24 information is feasible. Internet margin may also profit from the sale of Resi Lighting, driving margin enhancements.

[ad_2]

Source link

")

{kind=link}